Sustainability

Industrial expertise meets climate protection expertise.

Implement together.

Creating added value.

That is our motivation.

Has non-financial reporting already been carried out?

And what are the next steps?

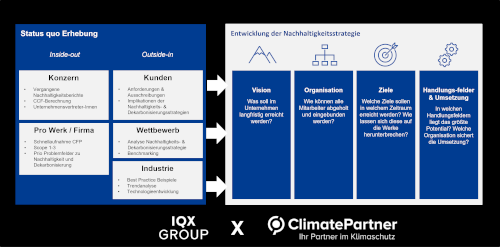

Together with our cooperation partner ClimatePartner, we want to enable a quick and cost-effective entry into this area. For us, calculating the CO2 footprint , developing the sustainability strategy, and actually preparing and approving the report by independent third parties are just the first steps.

Our expertise lies primarily in supporting your company in developing and effectively implementing decarbonization plans – including the necessary or possible measures related to buildings, machinery, and labor. A successful decarbonization plan requires minimizing all waste within the company, which can often lead to an improvement in business results.

Interested but don't feel like reading? Just contact me, I'm happy to help by phone or email.

Till Zöhrer

+43 676 970 41 14

This email address is stez protected from spambots. You need javaScript Enabled to view it.

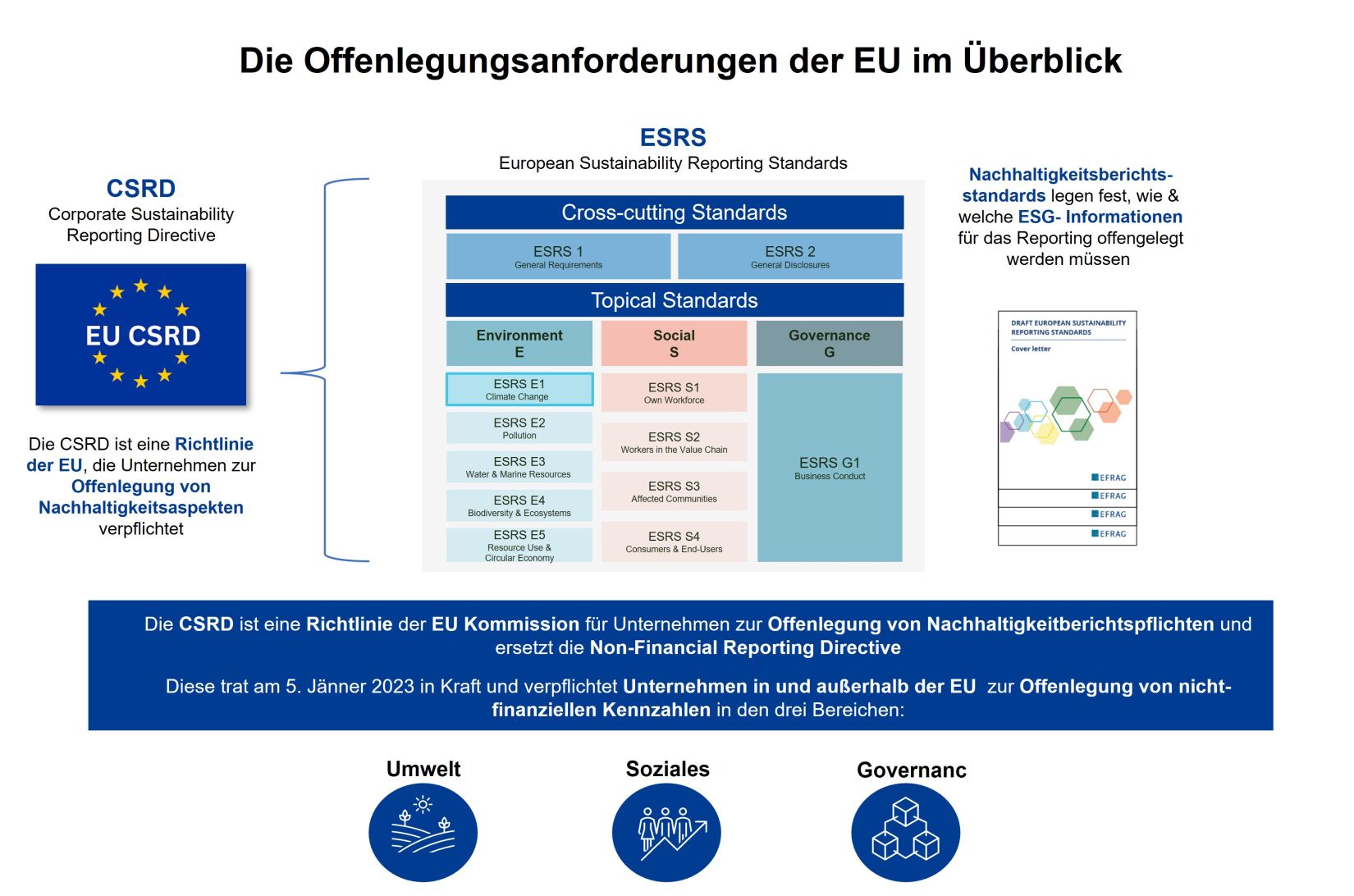

CSRD reporting is based on the concept of dual materiality – this means that companies must report on both material and financial impacts:

- Impact on materiality: Impacts that companies have on sustainability issues (e.g. CO2 footprint , employee rights, respect for human rights, …)

- Financial impact: The effects that sustainability issues have on companies' finances (e.g., liquidity, loss/profit, access to financing, risk, ...)

CSRD reports must be publicly available, and the CSRD requires third parties to verify the completeness of all disclosures.

Image: Our approach to the holistic implementation of the sustainability strategy in your company

Which companies must comply with the CSRD?

EU legislation has prescribed the following step-by-step plan for companies in the EU regarding the reporting obligation on SUSTAINABILITY by financial year.